Illinois Paycheck Calculator

Calculate your Illinois net check and take-home pay. Adjusts for federal income taxes, FICA withholding, pre-tax deductions, and Illinois' flat 4.95% state income tax.

Estimated Take-Home Pay

per bi-weekly pay period

Detailed Deductions Breakdown

How Much of an $85,000 Salary Do You Keep After Illinois Taxes?

Earning a salary in the Prairie State means navigating a flat state income tax rate of 4.95%, but without the standard deduction options found in many other states. For a single taxpayer bringing home a gross salary of $85,000 per year, this flat rate and the lack of standard deductions—offset slightly by a personal exemption—results in a net take-home salary of $64,565.

For professionals paid on a bi-weekly cycle—which yields 26 paychecks across the calendar year—this net package translates into a recurring deposit of approximately $2,483 per pay period.

This final net figure is calculated by subtracting federal income taxes (estimable using our Federal Paycheck Calculator), FICA withholdings, and Illinois flat state tax (SIT). To model custom deductions or run comparative scenarios, you can use our standard tools to run customized scenarios.

Illinois Take-Home Pay Snapshot

Below is the distribution of an $85,000 baseline annual salary for a single Illinois taxpayer.

Walking Through an Illinois Paycheck: A Step-by-Step Mathematical Example

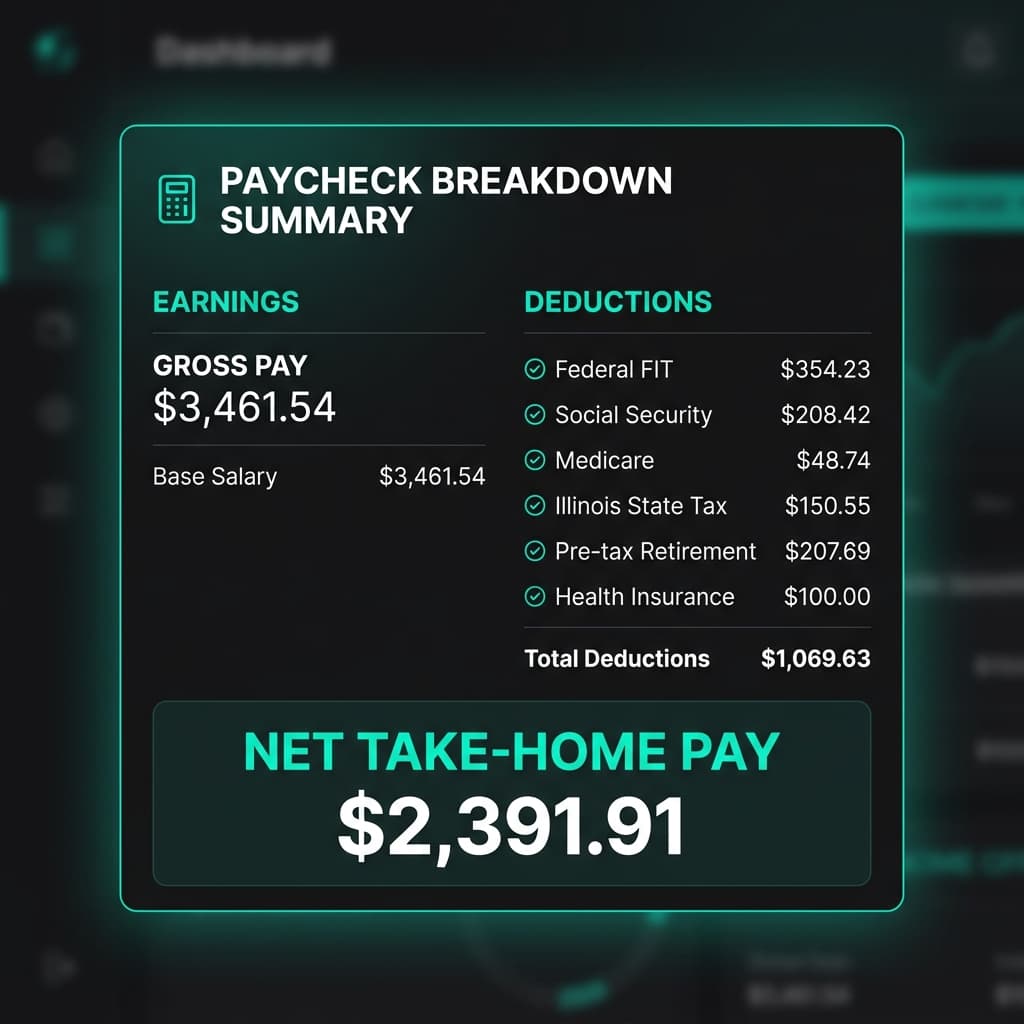

To see how these rules function on a real paycheck stub, let us follow a step-by-step example for an employee earning a gross annual salary of $90,000. This employee files as Single, works on a standard bi-weekly pay cycle (26 paychecks a year), contributes 6% of gross wages to a traditional pre-tax 401(k) ($207.69), and has $100.00 deducted per period for medical premiums.

This results in the following paycheck calculations:

- Gross Period Pay: $3,461.54

- Social Security (6.2% of FICA-taxable base): $208.42

- Medicare (1.45% of FICA-taxable base): $48.74

- Illinois State Income Tax (SIT - 4.95% flat): $150.55 (annualized to $3,914.22)

- Federal Income Tax withholding (FIT): $354.23 (annualized to $9,210)

- Total paycheck deductions: $1,069.63 (including pre-tax contributions and taxes)

- Net paycheck (Take-Home amount): $2,391.91

Why is There No Local Municipal Income Tax in Chicago or Cook County?

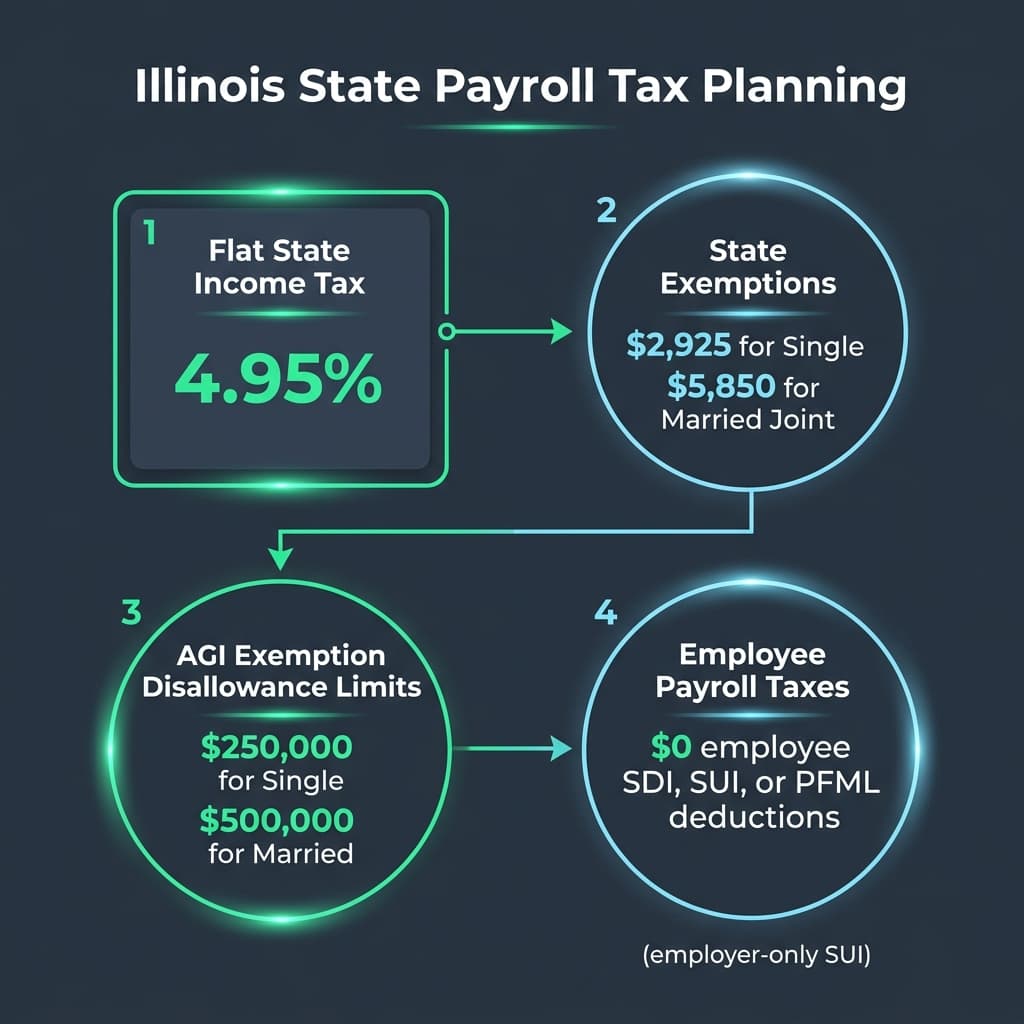

While many major cities in the Midwest and East Coast impose heavy local income taxes (such as municipal taxes in Philadelphia or occupational taxes in Alabama cities), Illinois taxpayers benefit from a constitutional restriction. Under the Illinois State Constitution, local governments, counties, and municipalities are strictly barred from levying their own individual income taxes.

Whether you work in the heart of Chicago (Cook County), Springfield, or Aurora, your municipal income tax rate is flat zero. Your state-level withholding is restricted solely to the flat 4.95% state income tax. This makes the overall payroll tax load highly competitive when compared to progressive states with heavy local surcharges like Delaware (up to 6.6% state tax) or progressive cities.

What Payroll Taxes for Disability or Family Leave Apply to Illinois Employees?

Employees in Illinois are exempt from worker-funded payroll deductions for state disability and paid family leave benefits. Unlike states such as Delaware (which levies 0.40% PFML) or California (which levies a 1.30% employee SDI tax), Illinois has no worker deductions for health, leave, or disability benefits.

Illinois' State Unemployment Insurance (SUI), also referred to as the reemployment tax, is paid exclusively by employers. Illinois employers pay this rate on a set taxable wage base for each employee. By law, no portion of this tax can be deducted from your paycheck. If you live or work in a state with no income tax at all, such as Florida, you will see even fewer withholdings on your paycheck.

How Do You Declare Allowances Using Illinois Form IL-W-4?

Your employer calculates Illinois state income tax withholding using the information provided on Form IL-W-4 (Employee’s Withholding Allowance Certificate), managed by the Illinois Department of Revenue.

Form IL-W-4 is used to document your state filing status and claim allowances for children or dependents. Because Illinois uses a flat tax system with an AGI phase-out, coordinating allowances is critical to preventing over-withholding. To coordinate your federal withholding, submit a separate Form W-4. For detailed information on employer unemployment filings, refer to the official portal of the Illinois Department of Employment Security.

Illinois Payroll Tax FAQs

Clear, expert answers to key questions about paycheck deductions, flat state tax rates, and withholding allowances in Illinois.

Other State Paycheck Calculators

Georgia Paycheck Calculator

Calculate take-home pay with Georgia's flat 4.99% tax rate and standard deductions of $15,000 / $30,000.

Delaware Paycheck Calculator

Calculate take-home pay with Delaware's progressive brackets (0% - 6.6%), personal credits, and 0.40% PFML.

Florida Paycheck Calculator

Calculate take-home pay in Florida with zero state income tax and zero employee disability deductions.

California Paycheck Calculator

Calculate payroll take-home pay in California with progressive SIT (1% - 13.3%) and 1.30% SDI deductions.